The Quiet Convergence of State Sovereignty and Private Digital Ledgers

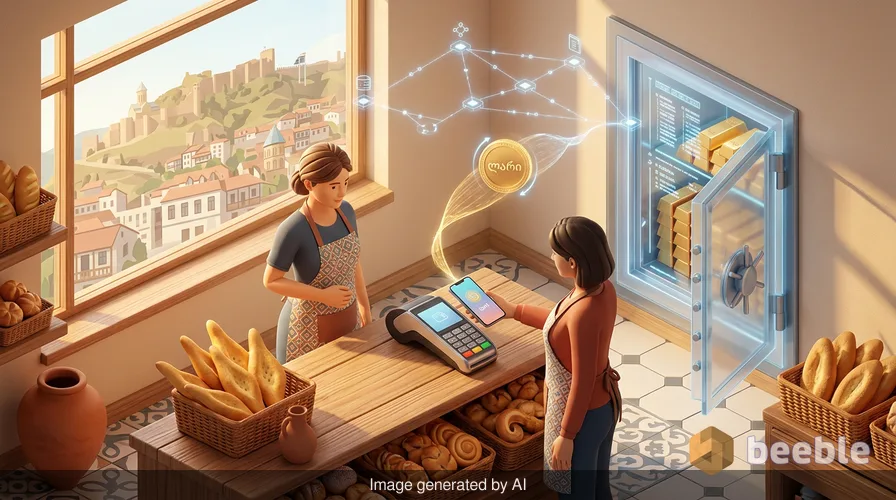

Imagine you are standing in a small, sun-drenched bakery in Tbilisi, the scent of fresh shoti bread filling the air. You reach into your pocket, but instead of pulling out a physical bank note adorned with the face of a Georgian poet, you tap your phone against a terminal. In an instant, a digital token representing the lari moves across a blockchain, settling a debt for a mundane purchase with the same finality once reserved for physical cash. This isn't a futuristic dream or a niche experiment for tech enthusiasts; it is the becoming reality of the Georgian financial system through a unique partnership between the world’s largest stablecoin issuer and a sovereign government.

Historically, the creation of money was the exclusive domain of the state—today, that authority is being shared with private code. In the past, the credibility of a currency rested solely on the military and economic might of the issuing nation; currently, that credibility is increasingly bolstered by the transparent auditability of a glass bank vault, where anyone can observe the reserves, yet only the rightful owner holds the key. This transition marks a profound shift in how we perceive the intersection of national identity and digital utility.

The Lari’s New Digital Shadow

Tether’s announcement that it will launch an "official" stablecoin in Georgia, dubbed GELT, represents a curious evolution in the world of digital assets. Unlike the traditional Tether (USDT), which acts as a global digital dollar, GELT is a digital representation of the Georgian lari, designed specifically to function within the nuances of the local economy. On an individual level, this means a resident of Georgia could soon hold their local currency in a digital wallet that is not tethered to a traditional bank account—this provides a level of financial mobility previously unavailable to the unbanked; however, it also introduces a private intermediary into the very heart of the nation’s monetary system.

Financially speaking, the term "official" carries significant weight, yet the details remains strikingly opaque. While the Georgian government and the National Bank have expressed vocal support for financial innovation, they have been carefully non-committal regarding the exact legal status of GELT. Is it a Central Bank Digital Currency (CBDC) in disguise, or is it merely a private product with a government blessing? To put it another way, Tether is attempting to bridge the gap between the wild west of crypto and the regulated halls of traditional finance, using Georgia as its primary laboratory for this experiment.

Why the Caucasus? The Logic of the Mining Hub

Georgia might seem like an unlikely pioneer for a global financial revolution, but zooming out, the country’s pro-crypto stance is deeply rooted in its structural advantages. For years, Georgia has been among the world’s top miners of cryptocurrency, driven by inexpensive hydroelectric power and a regulatory environment that views digital assets not as a threat, but as a path toward modernization. The National Bank of Georgia has even established specific stablecoin rules to attract businesses—this strategy turns the nation into a magnet for digital capital; conversely, it places the country at the center of a high-stakes geopolitical game where financial sovereignty is the ultimate prize.

In everyday terms, for the 3.7 million people living in Georgia, the arrival of GELT is less about global macroeconomics and more about the friction of daily life. For a small business owner in Batumi trying to order supplies from abroad, traditional cross-border payments can be slow, expensive, and buried under layers of bureaucratic red tape. A digital lari could theoretically slice through these hurdles, providing a streamlined path for commerce—this efficiency is the promise of the partnership; nevertheless, the risks of delegating currency issuance to a private, El Salvador-based company cannot be ignored.

The Paradox of Private Sovereignty

The Bank for International Settlements (BIS) has long warned that privately-issued stablecoins pose a systemic threat to monetary sovereignty. When a private company issues a token pegged to a national currency, it essentially creates a parallel money supply that the central bank cannot directly control. Historically, central banks used interest rates and money printing as levers to manage inflation and growth—in contrast, a world where private stablecoins dominate could render these traditional tools obsolete; consequently, the partnership in Georgia is a daring gamble on whether innovation can coexist with institutional authority.

Through this economic lens, we see a paradoxical shift in the nature of trust. We are moving away from a collective belief system backed by the state and toward a technical belief system backed by mathematics and collateral. Tether claims to have nearly $190 billion in circulation for its dollar-pegged token, a figure that rivals the reserves of many mid-sized countries. By launching GELT, Tether is not just offering a new product; it is expanding its influence into the very fabric of national economies—this expansion is pervasive and multifaceted; yet it remains vulnerable to the volatile whims of the global crypto market.

The Shadow of Previous Experiments

Not all of Tether’s regional experiments have been successes, which provides a necessary dose of skepticism. While their dollar-pegged token is ubiquitous, their attempts to launch tokens pegged to the Mexican peso and the offshore Chinese yuan have struggled with low demand and fragmented adoption. The Mexican peso token has less than $20 million in circulation, and the yuan token is being wound down entirely—this track record suggests that digital versions of local currencies are not a guaranteed success; instead, they depend entirely on whether the local population sees a tangible benefit over their existing banking apps.

On a macro level, Georgia is a different beast. Unlike Mexico or China, Georgia is actively inviting Tether into the fold, seeking to integrate the technology into its national payments infrastructure. This is symptomatic of a larger trend where smaller nations, feeling overlooked by the traditional global financial system, turn to blockchain as a way to leapfrog older technologies. Paradoxically, by embracing a decentralized technology, these states are seeking a more centralized form of digital control over their own economic destinies.

Behavioral Economics: Why We Choose Digital Wallets

As a journalist observing the behavioral patterns of retail investors, I often see a recurring theme: people don’t choose technology because they understand the whitepapers; they choose it because it solves a specific emotional or practical pain point. In many emerging markets, traditional banks are seen as opaque and restrictive—this creates a vacuum of trust that crypto companies are all too happy to fill. A digital wallet feels like a private sanctuary, a piece of the glass bank vault that belongs solely to the individual; meanwhile, a bank account often feels like a rented space subject to the whims of a distant manager.

However, this feeling of control can be a mirage. If the underlying stablecoin issuer faces a liquidity crisis, the digital tokens in that wallet could become worthless overnight. We have seen this market psychology play out repeatedly, where greed turns to fear in the blink of an eye—this cycle is as old as money itself; yet the speed of the digital age makes the impact more profound and interconnected than ever before.

Grounding the Innovation

Ultimately, the launch of GELT in Georgia is a litmus test for the future of money. If it succeeds, it could provide a blueprint for other small-to-mid-sized nations to digitize their economies without the massive overhead of building a proprietary CBDC. It represents a pragmatic alliance between the old world of sovereign states and the new world of decentralized finance—a hybrid model that acknowledges the power of blockchain while attempting to maintain the stability of the nation-state.

Practically speaking, for the average reader, the lesson here isn't to rush out and buy GELT or move to Tbilisi. Instead, it is an invitation to look at your own wallet and realize that the very nature of what you hold is shifting. The lines between your bank, your apps, and your government are blurring. As we move further into this digital era, the most valuable asset you can possess isn't a specific currency or a token, but a clear-eyed understanding of the systems that manage them.

As you navigate your next transaction—whether it’s a coffee at your local shop or an online purchase from across the globe—take a moment to consider the invisible plumbing beneath the surface. Is your money a physical promise from your government, or is it a digital entry on a private ledger? The answer is increasingly becoming "both," and how we manage that duality will define our financial lives for the next decade.

Sources

- Bank for International Settlements (BIS) Annual Economic Reports on Stablecoins and Monetary Sovereignty.

- National Bank of Georgia: Digital Asset Regulatory Framework and Stablecoin Guidelines.

- Tether Limited: Official Treasury Reports and GELT Project Announcements.

- Reuters: Financial Technology and Central Bank Digital Currency Analysis (2024-2026).

- World Bank: Georgia Economic Update and Cryptocurrency Mining Impact Study.

See you on the other side.

Our end-to-end encrypted email and cloud storage solution provides the most powerful means of secure data exchange, ensuring the safety and privacy of your data.

/ Create a free account