How an AI Agent Buying a 50-Cent Data Snippet Is Rewiring the Global Financial Infrastructure

The Friction of the Fifty-Cent Transaction

You have likely felt that subtle sting of annoyance when a website demands a five-dollar minimum purchase for a ninety-nine-cent digital download. Perhaps you were trying to access a single archived news article or buy a specific icon for a presentation, only to find yourself blocked by a payment gateway that deemed your small transaction “not worth the processing fee.” On an individual level, this is a minor frustration, a digital wall that forces us to either overspend or walk away. We are tethered to a legacy banking system that was designed for human-scale commerce—buying groceries, paying rent, or purchasing a car—where the overhead of verifying an identity and moving funds is baked into the price of doing business.

Now, imagine that frustration multiplied by a billion. This is the reality for the burgeoning world of artificial intelligence agents. These digital entities don't need groceries, but they do need data. They need access to specialized APIs, real-time weather feeds, and paywalled research to complete the tasks we set for them. Paradoxically, the very technology that represents the bleeding edge of human innovation has been, until recently, hamstrung by a financial plumbing system that dates back to the mid-twentieth century. For an AI to perform a task that costs a fraction of a penny, the traditional credit card network is simply too slow, too expensive, and too rigid.

The Invisible Wall of Traditional Banking

Historically, our financial systems have relied on a series of middlemen to establish trust. When you swipe a card, a complex dance occurs behind the scenes: your bank talks to the merchant’s bank, a payment processor verifies your balance, and a settlement network eventually moves the money days later. In practice, this works for humans because we operate on a relatively slow clock. We can wait three seconds for a terminal to beep or two days for a check to clear.

However, in the world of autonomous software, time is measured in milliseconds. From a consumer standpoint, we want our AI assistants to be seamless and instantaneous. If an agent has to wait for a manual credit card approval or deal with a “minimum spend” requirement every time it needs to ping a server, its utility evaporates. This systemic bottleneck has created a demand for a new kind of money—one that is machine-native, programmable, and settles instantly without the heavy baggage of traditional institutional oversight.

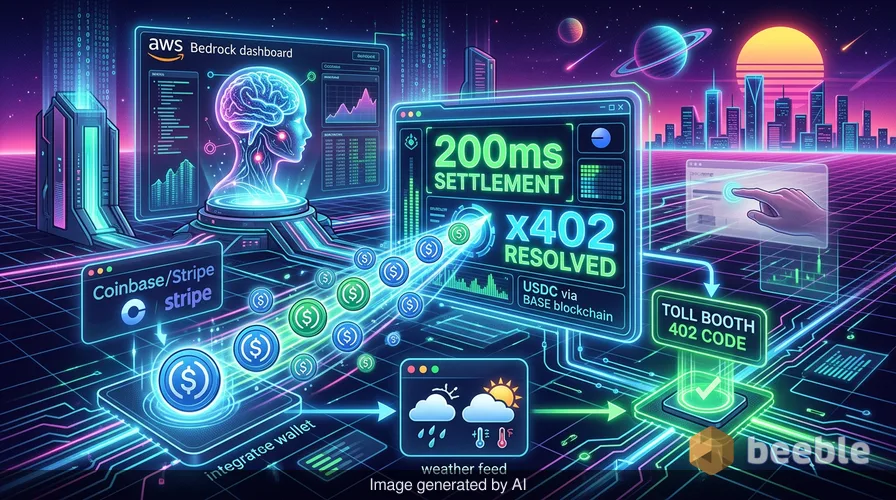

The AWS Solution: AgentCore and the x402 Protocol

This brings us to the recent announcement from Amazon Web Services (AWS). On a macro level, the launch of Amazon Bedrock AgentCore Payments, in collaboration with Coinbase and Stripe, marks a profound shift in how value is transferred across the internet. By integrating these systems, AWS is effectively giving AI agents their own digital wallets. This isn't just about adding a “Pay with Crypto” button; it is about building a framework where software can independently negotiate and execute transactions.

At its core, the system utilizes the x402 protocol, an open standard that leverages the existing HTTP “Payment Required” response code. Think of it as a digital toll booth. When an AI agent reaches a resource it needs to buy, the server sends back a 402 code. The agent, equipped with a Coinbase or Stripe-powered wallet, recognizes this signal and automatically sends the required payment in USDC—a stablecoin pegged to the U.S. dollar. Because these transactions happen on high-speed blockchains like Base or Solana, they settle in roughly 200 milliseconds. Curiously, this is faster than the blink of a human eye, allowing the AI to continue its task without a skip in processing.

Why Stablecoins Are the Digital Fuel of Choice

You might wonder why Amazon didn't simply use traditional dollars for this. The answer lies in the plumbing. Traditional fiat currency is a collective belief system supported by central banks and physical borders, but it is notoriously difficult to move across digital borders at high speeds. Stablecoins, through this economic lens, act as a bridge. They provide the price stability of the dollar with the technical agility of a blockchain.

Using a stablecoin like USDC turns the blockchain into a glass bank vault. Everyone can see that the funds are there and that the transaction was successful, but the underlying code ensures that only the intended recipient can access the “key” to the funds. This transparency is vital for enterprise security. For a company like Amazon, providing a managed solution means their developers don't have to build custom billing systems for every new AI tool they integrate. They can simply plug into the existing infrastructure and let the agents handle the accounting. Consequently, the barrier to entry for creating truly autonomous digital workers has just dropped significantly.

The Macro Shift: From Human Commerce to Machine Transactions

Zooming out, we are witnessing the birth of a machine-to-machine economy. For decades, the internet was a place where humans talked to machines to get things done. We are now entering an era where machines talk to machines to get things done on our behalf. This shift is symptomatic of a larger trend toward decentralization—the movement of control away from central hubs and toward the edges of the network.

When Coinbase reports that the x402 protocol has already processed over 169 million machine-native payments, it isn't just a speculative statistic. It is evidence of a new layer of global liquidity. In this world, money is no longer just a store of value; it is a line of code. This interconnected network of agents buying and selling services creates a level of efficiency that traditional markets can’t match. Paradoxically, while we often worry about AI taking jobs, the first thing it is actually taking over is the mundane administrative task of paying the bills.

The Behavioral Paradox of Autonomous Spending

Financially speaking, there is a nuanced psychological shift occurring here. As humans, we have an emotional relationship with spending. We feel the “pain of paying” when we hand over cash or see a large number leave our bank account. This emotional friction often acts as a natural brake on our spending habits. But what happens when that friction is removed?

When an AI agent spends money autonomously, the “pain of paying” is outsourced. From a behavioral economics perspective, this could lead to a fragmented understanding of our own finances. If your AI assistant is making hundreds of tiny, sub-cent purchases throughout the day—buying a weather update here, a traffic optimization there, a specialized translation service elsewhere—it becomes difficult for the average person to track where their money is going. Just as inflation acts as an invisible leak in your wallet, autonomous micro-spending could become a pervasive, quiet drain on our digital accounts if not properly managed.

Looking Ahead: When Your Assistant Books the Flight

Amazon has hinted that the future of this technology goes far beyond buying data snippets. Future versions of AgentCore could allow agents to book flights, reserve hotels, and complete complex retail purchases across various platforms. This represents a transition from “AI as a search engine” to “AI as a personal procurement officer.”

Ultimately, this moves us toward a world where our digital wallets are more active than we are. However, this level of autonomy requires a robust legal and compliance framework. As Brian Foster of Coinbase noted, many enterprises have been hesitant to let agents transact because of regulatory fears. By providing a managed, enterprise-grade solution, AWS is attempting to bridge the gap between the “Digital Wild West” of early crypto and the rigid requirements of Wall Street. It is an attempt to make machine-native payments as mundane and reliable as a credit card swipe, but with the power of a global, decentralized ledger.

Reclaiming Financial Mindfulness in an Automated World

As we stand on the precipice of this automated economy, it is worth pausing to reflect on our own relationship with digital money. We are moving toward a future where our spending is increasingly invisible, handled by algorithms that don't feel the sting of a budget deficit. While the efficiency gains of the AWS-Coinbase-Stripe partnership are tangible and profound, they also demand a new kind of financial mindfulness from us.

We must ask ourselves: How much autonomy are we willing to give our digital proxies? Do we trust the code as much as we trust the bank? As the lines between our personal finances and global blockchain indices continue to blur, the most valuable asset we have isn't the USDC in our wallets—it is our ability to remain conscious observers of the systems we build. In a world where machines handle the transactions, it remains our uniquely human responsibility to define the value of what we are buying.

Sources:

- Amazon Web Services: Official Announcement of Bedrock AgentCore Payments (May 2026).

- Coinbase Blog: The x402 Protocol and the Growth of Machine-to-Machine Payments.

- Stripe/Privy Technical Documentation: Wallet Infrastructure for AI Agents.

- Bitcoin Policy Institute: Study on AI Preference for Stablecoins and Bitcoin in Economic Simulations (March 2024).

See you on the other side.

Our end-to-end encrypted email and cloud storage solution provides the most powerful means of secure data exchange, ensuring the safety and privacy of your data.

/ Create a free account