Why is your Uber insurance fee so unpredictable?

Why did your last Uber to the airport cost twenty dollars more than the one you took last month? Most riders assume demand is the only culprit. However, a closer look at the receipt reveals a fee that fluctuates even when everything else remains constant. A recent analysis of trip data suggests that the line item for insurance and operations is far more volatile than the actual price of the ride. This lack of consistency raises questions about how much of your fare goes toward safety and how much is simply a flexible profit margin for the platform.

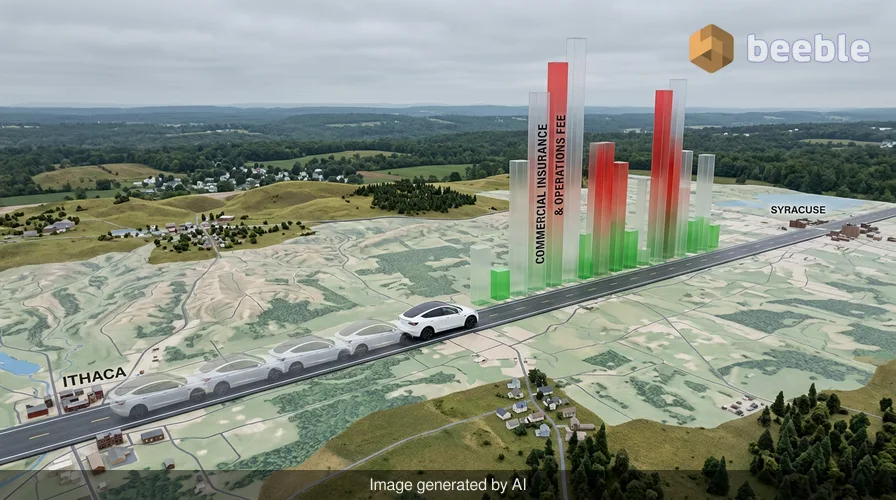

Len Sherman, a researcher at Columbia Business School, recently tracked 120 identical trips between Ithaca and Syracuse, New York. The parameters were remarkably stable. The same driver used the same Tesla Model Y to follow the same 60-mile route at similar times of day. Despite these identical conditions, the commercial insurance and operational charges reported by Uber swung wildly. On some days, the fee was as low as $13.75. On others, it spiked to $50. From a traditional risk standpoint, this variation makes little sense. If the driver, vehicle, and road conditions are the same, the cost to insure that specific trip should not quadruple overnight.

The mechanics of the hidden fee

Uber explains this volatility by pointing to the broad nature of its insurance obligations. An Uber spokesperson noted that these fees cover government-mandated insurance and can change based on the city of origin, the distance of the trip, the duration, and even the weather. However, the study found that the insurance fee was twice as volatile as the actual price riders paid for the trip. This suggests that the algorithm behind these fees is not just tracking the risk of a crash. It is likely balancing a complex ledger of internal costs that have nothing to do with the specific passenger in the backseat.

In everyday life, we expect insurance to be a predictable cost. You pay a set premium for your car or home because the risk is calculated over a long period. In the ride-hailing world, insurance acts more like a dynamic surcharge. Uber uses a mix of third-party providers and self-insurance, where the company sets aside its own cash to cover claims. Because Uber views these fees as an estimate rather than a direct reflection of a single trip, the money you pay for insurance on a Tuesday morning might actually be covering a claim from a different driver on a Friday night. Essentially, your fare is part of a massive, shifting pool of capital used to manage corporate risk.

Where the money goes

To understand the bigger picture, we can look at data from Gridwise, a platform that tracks earnings for gig workers. Their 2026 analysis shows that insurance now accounts for about 21% of the average ride-hailing fare. For a $50 ride, over $10 is swallowed by insurance costs before the driver or the platform takes their cut. The breakdown of a typical fare in early 2026 looks like this:

| Fare Component | Percentage of Total |

|---|---|

| Driver Earnings | 53% |

| Insurance and Operations | 21% |

| Platform Fee (Uber/Lyft Share) | 15% |

| Other (Taxes, Misc) | 11% |

Looking at the market side, insurance costs are actually falling in certain regions. In the Western United States, insurance expenses for ride-hailing companies dropped nearly 21% at the start of 2026. This was the result of California reducing its strict insurance requirements. Curiously, these savings did not result in a significant windfall for the people behind the wheel. While rider prices fell slightly and platform fees rose, driver pay only increased by a meager 1.2% on average. The savings from lower insurance costs stayed largely within the corporate ecosystem.

The disconnect between risk and price

For the average user, the insurance fee is a black box. Uber does not provide a detailed list of what counts as an operational expense. This category is a catch-all that can include anything from background check costs to the electricity bills for data centers. By bundling insurance with vague operations, the company gains the ability to adjust the total price of a ride without appearing to hike its own commission. When the insurance fee goes up, the company can claim it is simply responding to the high cost of protection, even if the driver is a five-star veteran with a perfect safety record.

This creates a systemic lack of transparency. Drivers can see the insurance breakdown in their weekly earnings summaries, but they have no way to contest a $50 fee on a trip that usually costs $15 to insure. The driver provides the car, the labor, and the primary risk of being on the road. Yet, they are the last to benefit when the cost of that risk goes down. From a consumer standpoint, you are paying a premium that feels arbitrary. If you take the same trip every day, you are essentially gambling on what the algorithm decides the insurance market looks like at that specific moment.

Shifting the perspective on ride costs

Ultimately, ride-hailing has evolved from a simple peer-to-peer service into a complex financial operation. The insurance and operational fee is the digital version of a fuel surcharge on an airline ticket. It is a flexible tool that allows the platform to maintain its margins while shielding itself from the volatility of the insurance market. The fact that an identical trip can have such a wide range of fees proves that the price is not tied to the reality of the road. It is tied to the needs of the platform's balance sheet.

Practically speaking, there is little a rider can do to change these fees, as they are baked into the upfront price. However, knowing that a fifth of your fare goes to an opaque insurance fund changes the value proposition of the service. Behind the jargon of commercial auto policy lies a simple truth: you are paying for more than just a ride from point A to point B. You are subsidizing a global risk-management machine that prioritizes its own stability over price consistency for the user. The next time you see a price jump on a clear day with no traffic, remember that the ghost in the machine might just be an insurance estimate working in the platform's favor.

Sources:

- Columbia Business School research by Len Sherman, 2026

- Gridwise Q1 2026 Market Analysis Report

- Business Insider investigation into Uber Reserve fee structures

- California Department of Insurance 2026 regulatory updates

See you on the other side.

Our end-to-end encrypted email and cloud storage solution provides the most powerful means of secure data exchange, ensuring the safety and privacy of your data.

/ Create a free account